IDX Composite :

Last Updated :

Last Updated :

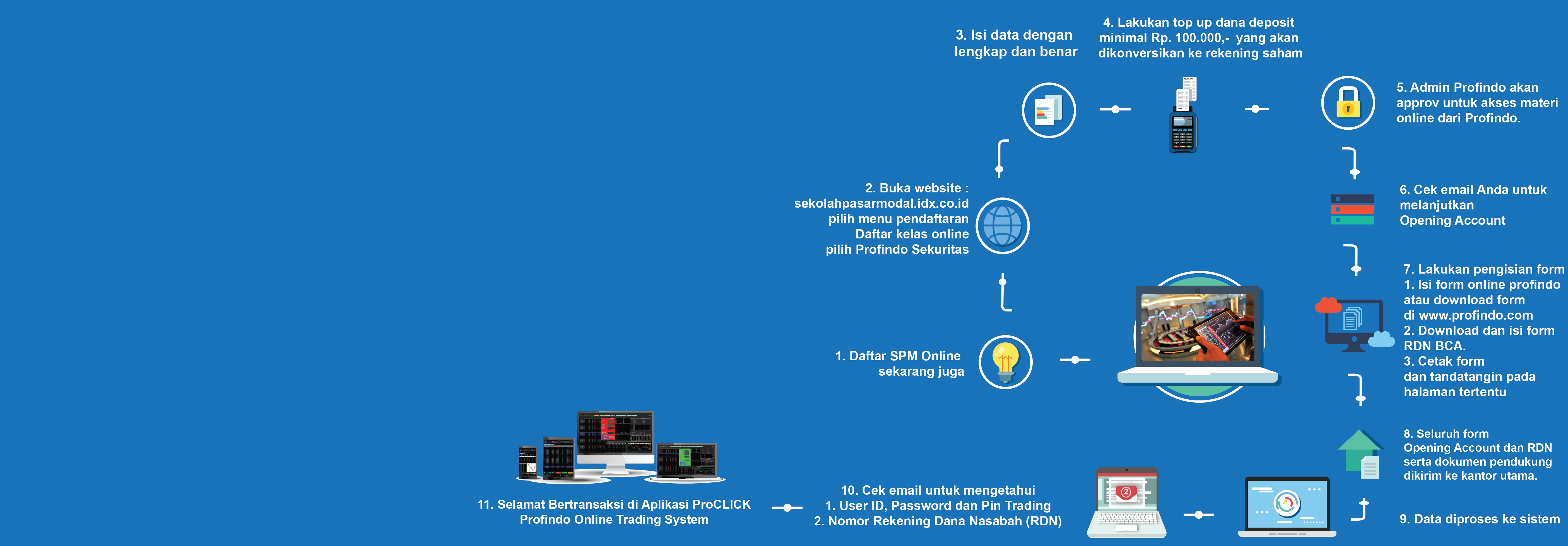

Reguler training will help us how to pick the best stock for all people especially for beginning investors. To maximize your understanding of stocks, we are prepare the dictionaries and more knowledge about education of capital market.

Reading is the key of success

Let’s us study right now

Equity Capital Market division offers Equity Brokerage as well as margin lending facility for retail, institutional and sophisticated investors.

Our Proclick® Online Trading Platform was created with user friendly system in mind. The platform allows investors to trade anywhere at their convenience.

Our Financial Advisory Team provide financial advisory service to help client tackle complex and challenging issue.

Investment Banking team will be able to help clients raising fund through public offering, bond offering, and placements.

Syarat dan Ketentuan Nasabah Perorangan

Diisi :

1. Isi dengan lengkap formulir pembukaan rekening efek dan Formulir Rekening Dana Nasabah (RDN);

2. Lampirkan dokumen pendukung yang disyaratkan, masing – masing 2 lembar dengan jelas, sebagai berikut:

a.) Fotokopi Kartu Tanda Penduduk (KTP) untuk WNI atau Paspor untuk WNA;

b.) Fotokopi Nomor Pokok Wajib Pajak (NPWP) atas nama pemilik rekening Efek/Pasangan/Orangtua;

c.) Fotokopi Kartu Mahasiswa (bagi Mahasiswa) yang masih berlaku;

d.) Fotokopi halaman pertama buku tabungan atas nama pemilik rekening efek;

3. Kembalikan Formulir Pembukaan Rekening Efek, Formulir RDN dan dokumen pendukung ke kantor utama.

PT. Profindo Sekuritas Indonesia (Up : Customer Service)

Head Office :

Gd. Permata Kuningan Lt. 19

Jl. Kuningan Mulia Kav. 9C,

Guntur Setiabudi, Jakarta Selatan 12980

Persayaratan Nasabah Institusi:

Notes: